Fintech for all: Mobile Money as a driver of Inclusive Growth in Africa

Since Safaricom’s 2007 launch of M-PESA in Kenya, mobile money has taken the African continent by storm.

As of December 2018, there were 395.7m registered mobile money subscribers across the continent, of which 145.8m were active. For the same year, the value of mobile money transactions across the continent amounted to $26.8 billion, representing over 65% of transactions globally. And in Kenya, where mobile money has become practically ubiquitous, the value of mobile money transactions amounted to nearly half of the country’s GDP.

Such a digital transformation has been a boon for many African economies. For businesses, mobile money has enabled new revenue streams, increased transparency and lower transaction costs. Its rise has also facilitated the formulation of many new ventures from ag-tech startups to e-commerce businesses. To give an example, in 2018 the value of e-commerce transactions using mobile money more than doubled across the continent.

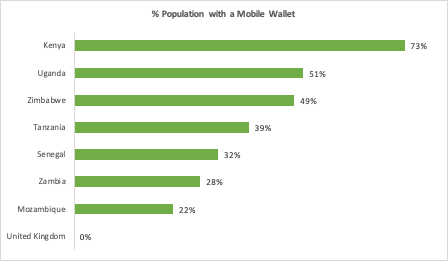

In the top chart a comparison of the % of mobile money subscribers across various countries in Sub-Saharan Africa. In the bottom chart, a comparison of % populations that have a bank account. (Source: Global Findex Database)

Governments have benefited too. At Kenya’s National Hospital Insurance Fund for instance, mobile money has reduced the workload of cashiers and other staff involved in cash collection, allowing staff to better focus their efforts on spreading further adoption of the national health insurance scheme. At a broader level, mobile money has the potential to save African governments billions every year through a reduction in leakages in tax collections and spending.

Mobile Money has had a major impact on average households

Perhaps most importantly, mobile money has had a significant impact on the livelihoods of every day African households.

Let’s start with daily cashflows. For many families, especially those who derive the bulk of their income from subsistence farming, income cycles are intermittent and uncertain. As such, one financial shock can throw an entire family into turmoil.

It in these difficult circumstances that mobile money proves most beneficial. Indeed, several studies undertaken over the last few years have underscored mobile money’s power to smooth out incomes and prevent families from sliding into transient poverty. For those familiar with Africa, this should come as no surprise. Many families depend on remittances from friends and family; mobile money has made it easier than ever for them to send and receive money.

MTN Smart T, a KaiOS device supporting smartphone apps and functionality and processes.

Image credit: Wiza Jalakasi

In a study conducted in 2016, the authors found that Ugandan households with mobile money accounts were 20% more likely to receive remittances and received a total value of remittances that was 30% greater than for non-user households. Households that receive more remittances can in turn increase consumption and better save for the future. And they will also be less likely to take out loans to fund basic necessities in times of crisis.

Beyond improving income cycles, mobile money is slowly moving average households up the financial services ladder. A farmer can now more easily get access to credit to purchase seeds and fertilizer and sign up and pay for crop insurance to protect himself against a poor harvest; a mother now has access to solar at a lower price, which she can pay for using mobile money, providing her family with reliable power at home; and all households can now securely save cash using their phones. In our analysis, improved access to financial services for more underserved populations occurs once a critical mass of mobile money subscribers in a particular country is reached.

TWA Analysis: The Stages of Mobile Money growth for financial services access

Mobile Money usage will continue to grow across Africa

Mobile money still has a long way to go—its usage is still limited in most parts of Africa, save for a few countries in East Africa. But that is changing fast, as governments, multilaterals and foundations ramp up their support for its development in more underserved markets. One such example is Mobile Money for the Poor (MM4P), an initiative launched in 2012 and supported by various funders such as the United Nations Capital Development Fund and the MasterCard Foundation, which has so far reached 8 million new mobile money subscribers across 7 countries.

Growth in mobile money accounts across several African countries between 2014-2017. (Source: IMF Financial Access Survey)

The value of transactions has grown 890% since 2011 and will likely continue to grow exponentially. Such growth in digital finance provides African countries with the opportunity to add as much as 12% to their GDPs. And more importantly, it offers countries the opportunity to foster inclusive and sustainable growth

At Third Way, we are excited to see what the future holds for fintech in Africa and believe in the power of mobile money to foster financial inclusion and open opportunities for all Africans, from businessmen to small-holder farmers.