Financing productivity: the role of asset-based finance in unlocking agricultural growth across Sub-Saharan Africa

MSMEs are crucial drivers of livelihoods, economy, and food security in Sub-Saharan Africa – but they remain largely under-financed

SMEs are estimated to contribute more than 50% of African GDP and an average of 60% of employment. The MSME finance gap (or the percentage of formal MSMEs that cannot or can only partially access credit) is estimated at 51% for sub-Saharan Africa, the highest regional percentage in the developing world. In the agricultural sector, where climate and supply chain risks are material, the picture is starker: an estimated 83% of agri-SME financing needs go unmet. Ensuring these businesses thrive safeguards employment (including opportunities for women and youth) as well as food security.

Despite more than a decade of donor programmes, government schemes, and private-sector initiatives, the shortfall has continued to widen. Today, the MSME finance gap in emerging markets and developing economies stands at US$5.7 trillion, and the gap in Sub-Saharan Africa alone is equivalent to approximately 20% of GDP.

Stringent collateral requirements are a core barrier to financial inclusion in Sub-Saharan Africa (SSA)

Lack of collateral is often cited as the primary barrier to finance for MSMEs in Sub-Saharan Africa. Financial institutions typically seek hard, legally enforceable collateral such as titled land, buildings, and vehicles — requirements which many agri-SMEs do not have. Women-owned MSMEs, in particular, are less likely to own titled land or fixed assets due to legal and cultural barriers. Only around 13% of women in Sub-Saharan Africa claim sole ownership of land compared with 36% of men.

Limited access to assets – particularly productive assets – plays a role not only in the Sub-Saharan MSME finance gap, but also in the larger agricultural productivity gap

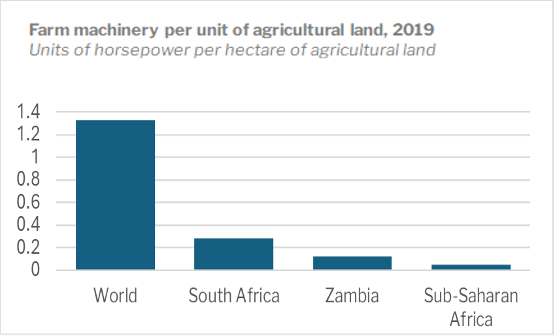

For agricultural businesses, limited ownership of assets for collateral is not only constraining access to finance for MSMEs but also productivity. In fact, African cereal yields average roughly half of the global average – a gap generally attributed to four structural factors: fertiliser use, agronomic knowledge, irrigation, and mechanisation.

Deployed alongside those other factors, mechanized technologies such as tractors, driers, crushers, small-scale irrigation, and motorised transport raise productivity, save labour, cut post-harvest losses and build climate resilience. Today, approximately 60% of African farmland is still cultivated manually, with only about 10% of agricultural power sourced from tractors or motorised equipment. Where these technologies are available, they often remain out of reach: supply is thin and fragmented, imported equipment and spare parts are expensive, and without finance, the upfront cost is simply unaffordable for most smallholders and other agri-SMEs.

Evidence of mechanisation-led productivity in Sub-Saharan Africa (SSA)

Mechanisation is not a silver bullet on its own. The gains materialise only when equipment is matched to the right crop and context, used well, and combined with the other factors above. That said, the benefits of mechanisation have been documented across the region:

In Zambia, mechanised households earned roughly twice the income of non-mechanised households.

In Ethiopia's Arsi Zone, adoption of agricultural machinery raised farm income by around 70% and cut the likelihood of food insecurity by about 51%.

The effect on scale is just as striking: a farm family relying on human power alone can typically cultivate about 1.5 hectares a year, rising to roughly 4 hectares with draught animals and to more than 8 hectares once a tractor is available.

A four-country study spanning Benin, Kenya, Nigeria and Mali found that farmers themselves attribute higher yields to mechanisation through reduced labour shortages, better timeliness and improved land preparation, alongside higher incomes and a marked reduction in drudgery that frees up time for other farm and off-farm activities

Asset-based finance can expand financial inclusion and drive agricultural productivity

Asset finance, and equipment leasing in particular, does two things at once. It expands financial inclusion — the asset itself serves as security, so a smallholder or rural enterprise can borrow without titled land. It also drives mechanisation and productivity, with knock-on effects for food security and climate resilience: more stable rural incomes help households absorb shocks when harvests fail. Modern, resource-efficient equipment can also support adaptation and lower the emissions intensity of production.

What is asset-based finance?

Asset finance lets a business/ borrower obtain the use of an asset and spread its cost over time, with the asset itself serving as security. Structures range across a spectrum from use to ownership: an operating lease provides temporary use with the asset returned at the end; a finance lease transfers substantially all the risks and rewards of ownership to the customer; and lease-to-own (hire purchase) grants use through scheduled payments, with title passing to the customer after a final payment.

Key challenges with the traditional approach to asset-based finance

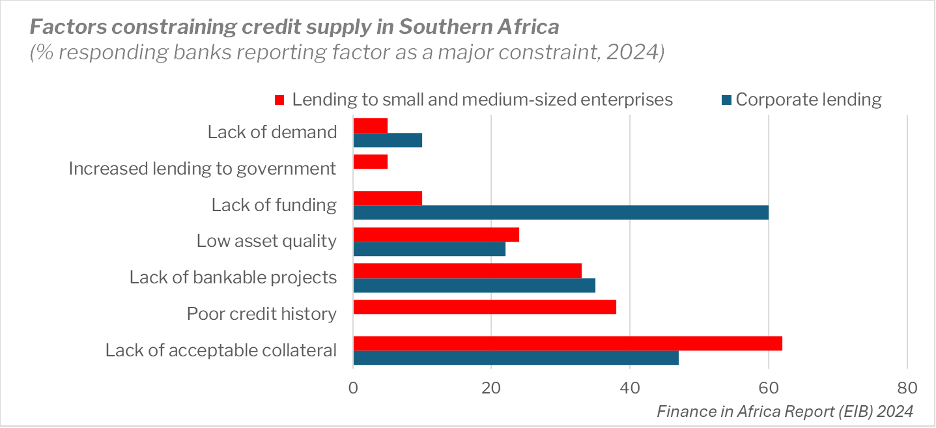

ThirdWay Partners’ work with banks, non-bank financial institutions (NBFIs), development organisations and equipment providers across Southern and Eastern Africa has shaped a clear view of where the model struggles in practice. First, most traditional lenders are not equipped to assess asset-based risk: farmers and agri-SMEs often lack formal credit histories, and lenders have little visibility into how an asset is used or maintained. As a result, risk is poorly understood and overpriced into higher rates and shorter tenors. Second, recovery is weak: with no developed secondary market for used equipment and little appetite to remarket repossessed assets, lenders cannot reliably turn collateral back into value. Third, the finance on offer is the wrong shape: predominantly short-term and working-capital-oriented, it is ill-suited to productive assets, which need larger tickets, longer tenors and repayments matched to the asset's payback period. Underlying all three, asset finance is operationally intensive — demanding client education, asset selection and after-sales support that are costly to scale in rural markets. The insights below shed some light on how different actors in the space are addressing these gaps to make asset-based finance work in practice for rural SSA.

Insights from TWPs work with asset-based finance across Sub-Saharan Africa

1. Ensure demand is anchored in real use case

Asset-based finance is only effective when the product is anchored in the real productive use cases of specific businesses, not in standardised offerings or top-down programme assumptions. Farmers and agri-SMEs do not demand “asset finance” in abstract terms—they require particular assets that solve binding constraints, whether irrigation, cold storage, mechanisation, or processing equipment.

Development interventions should therefore avoid prescribing asset categories or product structures upfront, working iteratively with businesses and market actors to identify the assets that drive productivity and income in practice.

Learnings from an MFI asset-based finance programme in Zimbabwe

TWP helped an NGO in Zimbabwe upskill MFIs to reach rural, informal women entrepreneurs, which shed light on how demand for assets forms in rural markets and how to build sustainable matching-grant asset-finance products.

First, demand is socially anchored. Farmers build conviction by watching what their neighbours use successfully, not from generic product offers. Partnerships work best when built around trusted local suppliers who already carry the brand recognition and after-sales presence that underpin client confidence.

Second, stated preferences are not effective demand. The initial programme was built around a survey of what businesses said they wanted, yet the resulting assets went untaken because they proved too expensive, and stringent program-level rules on eligible asset types and target group left the product mismatched to real demand. Market analysis must test affordability and use case before design, not just record what businesses say they want.

Third, concessional capital should make a product commercially sustainable, not just cheaper. Buying down the asset price flatters uptake but collapses once funding ends and crowds out the price discovery that proves a product can stand alone. More durable approaches use subsidy to share early risk while the model proves itself, through results-based or blended structures that catalyse commercial capital rather than substitute for it.

2. Underwriting must reflect asset economics

Traditional lending focuses on the borrower: credit history, collateral, financial statements. Asset-based finance flips the lens to the asset, considering how the asset works, where it fits the value chain, and whether it can generate the cash flow to repay.

This demands deeper expertise than most lenders have today. Cost is the easy part; they also need to grasp how the asset is used, what it costs to maintain, and what income it can generate. Financing an irrigation system, for instance, means understanding crop cycles, water access and likely yield gains.

Effective models therefore assess asset-level cash flows, align repayment to income cycles, and incorporate mechanisms to monitor performance over time.

This means that equipment providers are a critical chain in the link. They know how assets perform in practice, have visibility into client usage, and can judge whether an asset suits a given business. Building that expertise into underwriting is essential both to expand access and to ensure financed assets are genuinely productive.

Across Sub-Saharan Africa, a new generation of specialist asset-leasing companies (often operating as non-bank financial institutions or NBFIs) is emerging to fill the gap that commercial banks have struggled to close. Unlike traditional lenders, these NBFIs are built around the asset rather than the borrower: their underwriting, servicing and recovery infrastructure is designed for equipment lifecycles, not balance-sheet collateral.

Equipment leasing company example: EFAfrica Group (EFAG).

EFAG offers a concrete illustration. Across more than a decade in Tanzania and a more recent presence in Kenya and Zambia, EFAG provides leases for productive assets — such as irrigation and processing kits, transport and logistics equipment — without additional collateral or large upfront cash outlays. Roughly 75% of EFAG’s leases have gone to smallholder farmers and MSMEs, and the company has generated approximately 12,000 jobs in the markets it operates in.

Rather than asking what a borrower already owns, EFAG underwrites the income the financed asset is expected to generate, sizing repayments against the asset's own productive cash flow. Years of lending on the ground have given EFAG its own intellectual property in credit-scoring and product design, grounded in direct client relationships and supplier connections. This allows EFAG to appraise applications far faster than a traditional bank and offer repayment terms matched to clients' cash flows. Supplier due diligence validates that each asset fits the client's use case before disbursement, the asset itself serves as security, and ongoing monitoring tracks performance afterwards, giving EFAG visibility and recovery options conventional lenders lack. The financing comes bundled with fintech-enabled credit appraisal, user training and equipment maintenance, wrapping the asset in the support a client needs to use it productively and keep repaying.

For many clients, EFAG fills a genuine market gap: 80% had not previously accessed similar equipment and 71% could not identify a good alternative. Once acquired, the equipment improved operations: 86% of clients reported better business performance through more timely land preparation, expanded cultivated area, reduced transport bottlenecks, and more reliable service delivery. These operational gains translated into income and employment effects, with most clients reporting revenue growth and 76% hiring seasonal workers. Importantly, the impact often extended beyond the direct borrower, as clients rented out tractors, tillers, and vehicles or provided ploughing, transport, and crop-purchasing services to neighbouring farmers and businesses.

In this sense, EFAG’s model demonstrates how productive assets can function as shared rural infrastructure, strengthening local value chains, livelihoods, and resilience in climate-exposed rural economies.

3. Risk must be structured and shared

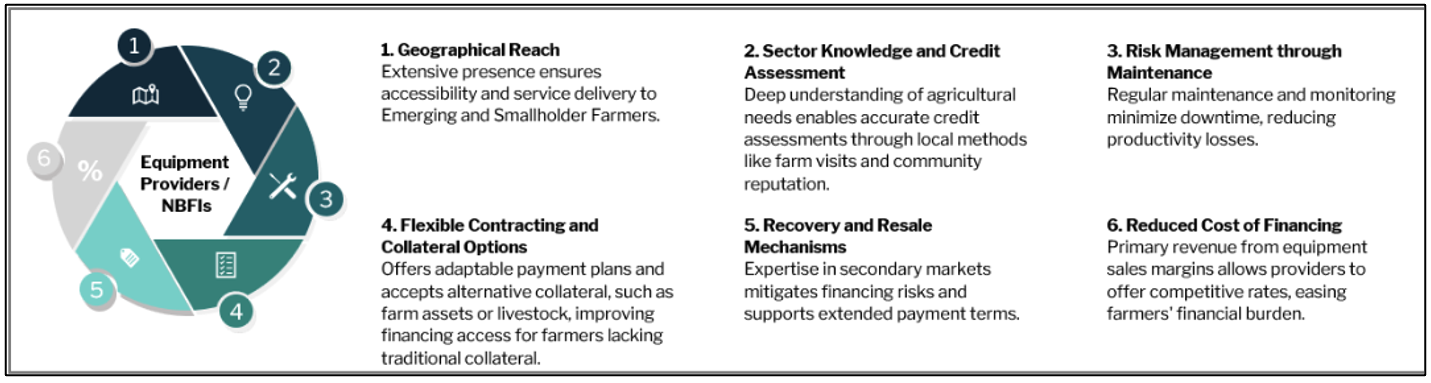

ThirdWay Partners has supported the development of innovative partnership models that link traditional financial institutions with equipment providers and asset suppliers in Sub-Saharan Africa, recognising that asset finance cannot be delivered effectively by lenders alone. Equipment providers bring exactly what FIs lack: a physical presence close to end-users, deep sector knowledge, and a commercial incentive to see the asset succeed — because their margin comes from selling and servicing equipment, not from interest.

In traditional models, financial institutions originate the loan, carry full credit risk, and have limited visibility or control over how the asset performs post-disbursement. This creates a fundamental misalignment between risk and control. By contrast, structured asset finance models can redistribute roles more effectively:

financial institutions (FIs) provide capital and manage the portfolio

equipment providers anchor the model: their existing geographic proximity to farmers and agronomic knowledge let them appraise and price risk more accurately through field visits, they validate asset suitability at origination, and they stay involved through maintenance, monitoring and, where needed, recovery and resale into a market they understand, the very capabilities most FIs lack

Incentives and risk can be explicitly shared between FIs and equipment providers, aligning incentives across both parties. For instance, risk-sharing agreements where equipment providers split the losses on any defaulted loans. On the incentives side, because an equipment provider earns from selling and servicing assets rather than interest, it has every reason to keep clients productive and repaying — and can often support lower rates than a bank while co-financing alongside the lender to share risk directly. The result is a stronger model overall: risk is managed through partnership rather than carried by the lender alone, and pricing reflects shared control instead of a mark-up for weak collateral and limited visibility.

Deep dive: Addressing the collateral constraint for agri-SMEs in Zambia

In Zambia, MSMEs account for approximately 97% of businesses and contribute 70% of gross GDP. Despite this clear economic importance, MSMEs face persistent constraints to growth, and access to finance sits near the top of the list. Zambia illustrates, in microcosm, how the collateral barrier translates into a productivity gap and how the right financing structure can begin to close it.

The evidence shows how few of these businesses ever reach formal credit. Between 2017 and 2022, less than 10% of MSMEs reported applying for a loan from formal or informal sources, falling to just 5% among rural MSMEs. About a quarter of those MSMEs that did not apply cited high interest rates or lack of collateral as deterring factors, and for those who applied and were rejected, lack of security or collateral was the primary known reason for denial (22% of MSMEs). Collateral, in other words, is not a marginal hurdle but a central gatekeeper, deterring many businesses before they apply and blocking a further share at the point of decision.

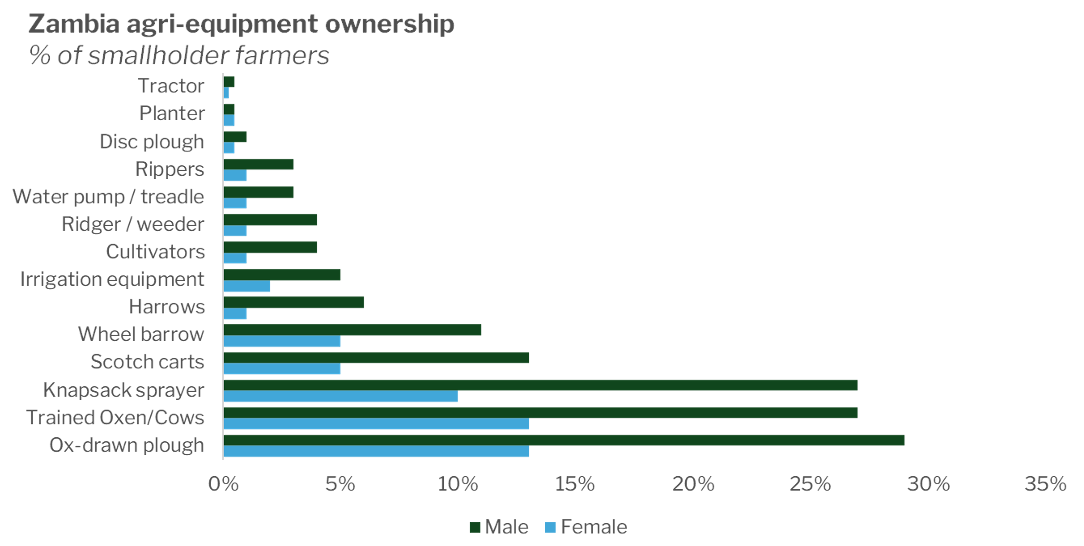

The same collateral gap is visible in data reflecting what producers actually own. As the chart below shows, ownership of productive equipment among smallholder farmers is extremely low. Powered and mechanised assets barely register: tractors are owned by well under 1% of smallholders, and irrigation equipment and water pumps by only a few percent. The irrigation gap in particular leaves the majority of farmers exposed to the rainfall variability that climate change is intensifying. Furthermore, women own less than men across almost every category.

Rural Livelihoods Survey 2019

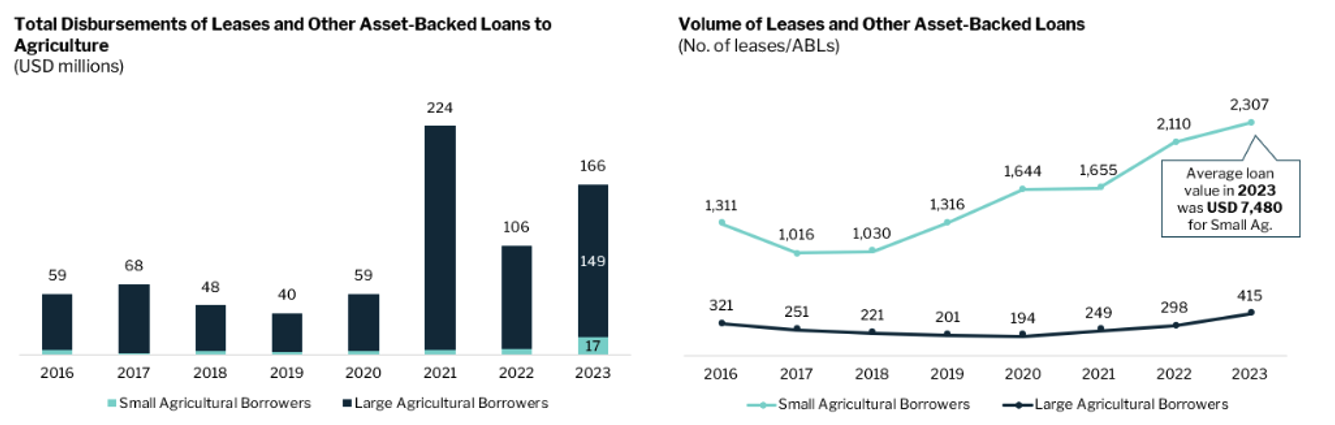

Encouragingly, asset-backed finance is increasingly reaching the very borrowers traditional credit leaves out. As the chart below shows, small-scale agricultural borrowers now make up the large majority of leases and asset-backed loans by volume, and their share has risen steadily since 2018 as the channel has matured — evidence that, structured well, asset finance can bring excluded agri-SMEs into the formal financial system. Ticket sizes remain small, in the order of a few thousand US dollars each, reflecting the modest scale of individual smallholdings rather than any ceiling on demand.

One company driving innovation in this space in Zambia is AgLeaseCo — a Bank of Zambia-licensed non-bank financial institution that began operating in 2017, backed by KfW Development Bank and the Africa Agricultural Trade and Investment Fund. Its lease-to-own model provides agricultural equipment directly to small-scale and emerging farmers, precisely the segment that dominates asset finance by number yet has long been excluded from conventional credit. Crucially, it requires no titled land or additional collateral: the leased equipment is the only security, so a farmer working customary land with no formal documents can still access a tractor, irrigation kit or processing machine. Fixed local-currency leases run for two to five years, are priced far below the rates typical of microfinance lenders, and farmers can buy the asset outright at the end of the term. The model is built on a network of established equipment suppliers who handle selection and after-sales service. These suppliers co-finance alongside AgLeaseCo, reinforcing responsible sales and risk monitoring. The model has also deliberately reached women farmers — a dedicated two-wheel-tractor scheme helped lift their share to more than a third of the portfolio.

Conclusion

Asset-based finance offers a practical route around the collateral barrier that keeps agricultural MSMEs out of formal credit: the financed equipment serves as both security and the source of repayment, and that same equipment raises yields and incomes. But the evidence in this article points to a narrower conclusion than “more leasing.” The model delivers only when it is built around the client — the right assets matched to a real use case, underwritten against the cash flow they generate, and wrapped in the services that keep them productive: training, maintenance, after-sales support and active monitoring. Where those capabilities are missing, finance can be mispriced, assets may sit idle or misused, and borrowers can over-commit.

This has a direct implication for concessional capital providers. The binding constraint is no longer proof of concept but institutional capability — in lenders, equipment suppliers and the partnerships between them. Concessional capital is best spent building that capability and sharing early risk while commercial models mature. Used this way, subsidy catalyses durable, commercially viable asset finance instead of substituting for it.