Predictability Is Policy: Why rules beat discretion in agricultural markets

Agricultural markets are inherently risky. Weather variability, price fluctuations, and external shocks are built into the sector. What market actors consistently struggle to manage is not natural risk but policy uncertainty.

Across several agricultural reform processes we have supported in Southern Africa, one pattern appears repeatedly: where rules are unclear or applied inconsistently, investment slows, informality rises, and years of strong production fail to translate into sustained growth. This is true even where governments are actively pursuing food security and farmer support objectives.

The problem is rarely a lack of policy. It is the unpredictability of how policy is applied.

What a well-functioning market requires

It is worth being clear about what predictable rules are and are not. Predictability is not simply about having rules written down. It is about whether market actors, farmers, traders, processors, financiers, can rely on those rules being applied consistently, and whether they can understand in advance the conditions under which government will intervene.

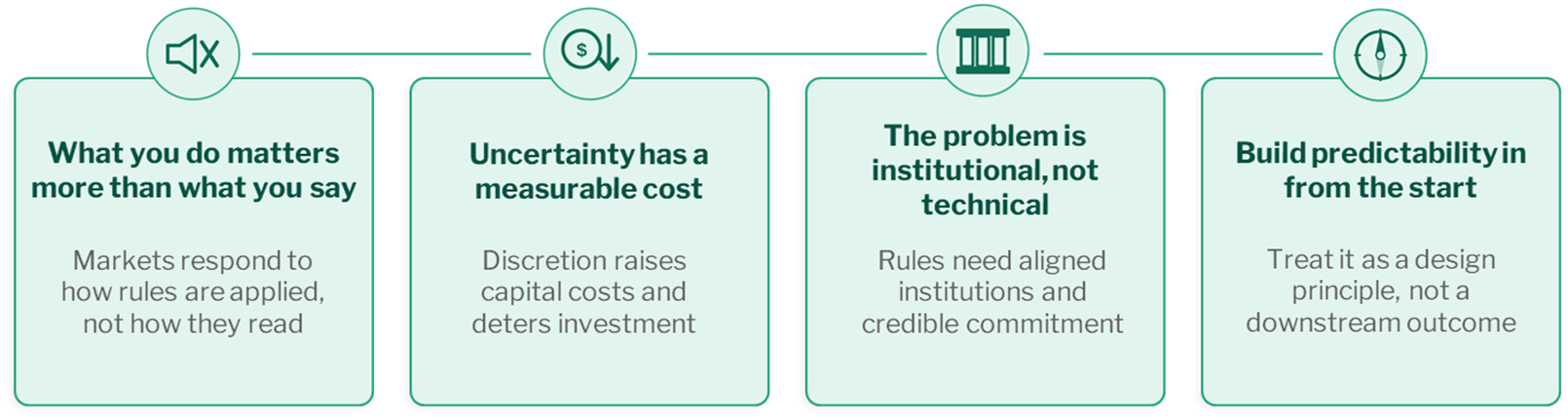

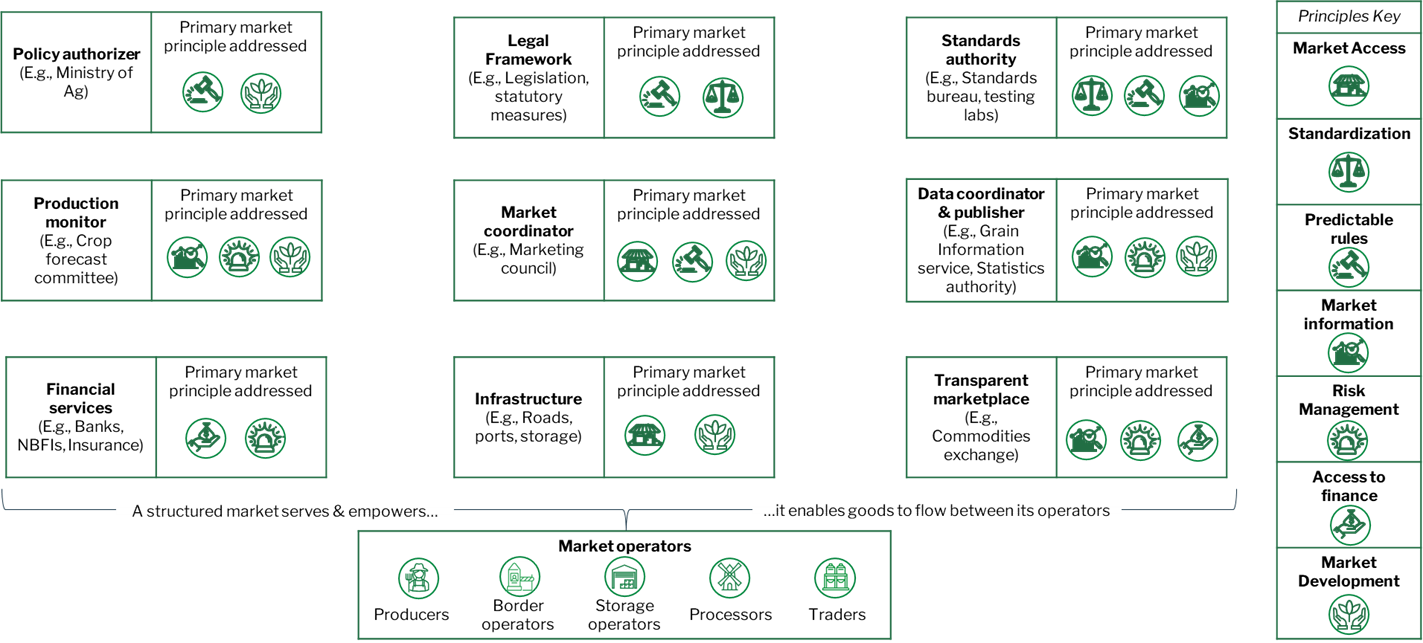

Our analytical work across Southern African grain markets points to seven core principles that structured agricultural markets need to function: market access, standardisation, predictable rules, market information, risk management, access to finance, and market development. These are interdependent. Weaknesses in any one of the principles constrain the others.

The seven principles of a structured agricultural market, predictable rules sit at the centre of a system that depends on all seven functioning together.

Predictable rules are not an optional extra in this system. They are the mechanism through which price discovery functions, through which investment decisions are made, and through which the other six principles become operational. Without them, access to finance becomes speculative, market information loses its decision-making value, and risk management tools lose their credibility.

Markets respond to behaviour, not announcements

Policy intent matters, but markets respond to behaviour. Farmers, traders, processors, and financiers make decisions based on how policies have been applied in the past and what they expect will happen next.

Across an entire agricultural sector ecosystem, different actor/segments of the sector will have responsibility to ensure implementation or protection of some of these key principles.

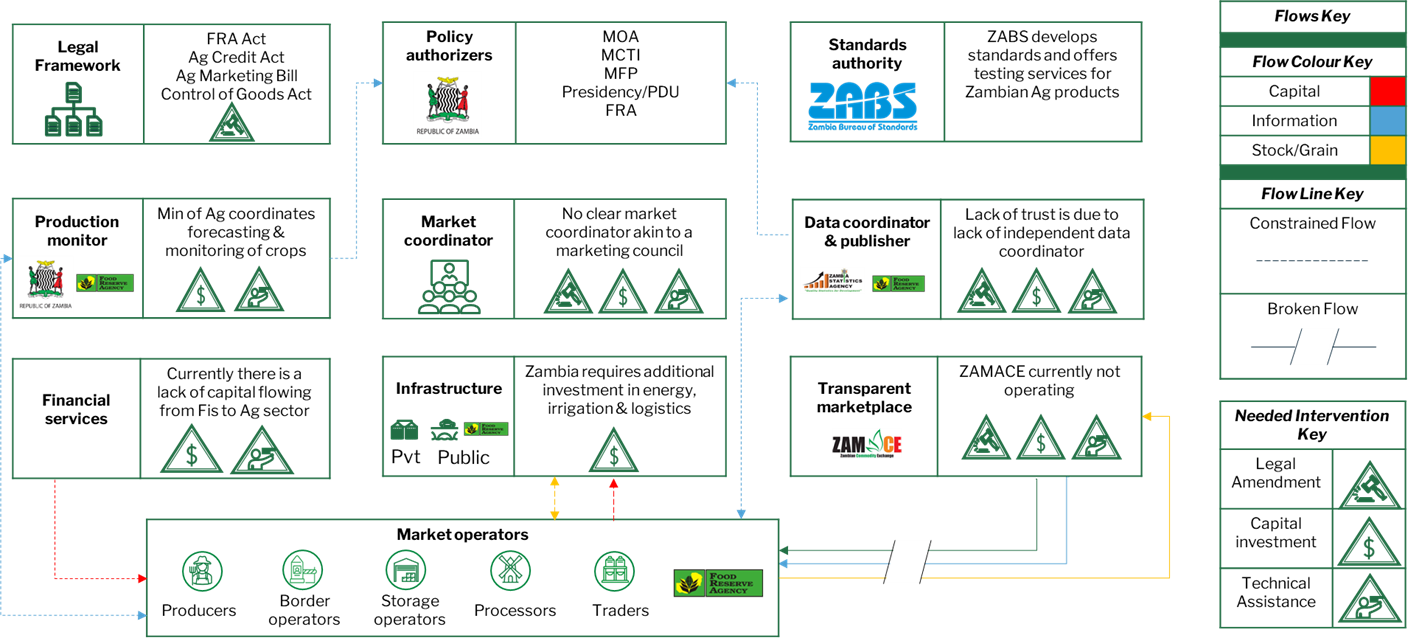

In Zambia, the key actors responsible for setting and enforcing these predictable rules included government agencies and standards authorities. Our observations showed that there were clear breakages between these rule setters and enforcers, and the market actors who need to act in accordance with them, not to mention key market players, like a marketing council, not being present at all.

Across the whole Zambian agricultural sector ecosystem, several breakdowns between key market actors/instruments has led to lack of enforcement of the structure agricultural market principles discussed above.

One of the key constraints identified that was significantly infringing on the principle of predictable rules was the unpredictable and often sudden use of export bans for maize. and public sector participation. Our diagnostic work across the Zambian identified these bans as one of the most significant structural constraints, not because the bans themselves were always wrong in intent, but because their application was difficult to anticipate.

When discretionary interventions are frequent or difficult to anticipate, private actors tend to reduce exposure, delay investment, or shift activity into informal channels. The result is often a paradox. Interventions designed to stabilise markets can end up amplifying volatility by discouraging the very private activity needed to absorb shocks. Governments intervene to protect farmers and consumers; markets interpret that intervention as a signal of further unpredictability and pull back. It is important to note that since this initial analysis was done significant progress has been made in Zambia to move towards a more structured, predictable agricultural market. The current reform progress is well underway, with three crucial Bills making there way through Parliament. Once completed, new process, institutions and obligations to report and share data will greatly enhance the predictability of Zambian agricultural markets.

Discretion carries hidden costs

Discretionary policy tools are attractive because they appear flexible. They allow governments to respond quickly to emerging challenges and adjust interventions as conditions change. In practice, discretion often carries costs that are less visible but no less real.

Uncertainty increases transaction risk, raises the cost of capital, and weakens incentives to invest in storage, logistics, and processing capacity. Over time, this erodes the structural resilience of agricultural markets and reduces the very resilience that would otherwise help governments respond to food security shocks without having to intervene in the first place.

In several reform processes we have supported, stakeholders consistently raised the same concern. It was not the fact of government intervention that unsettled private actors. It was the absence of clarity around when, how, and for how long that intervention would be applied.

The evidence from across the continent

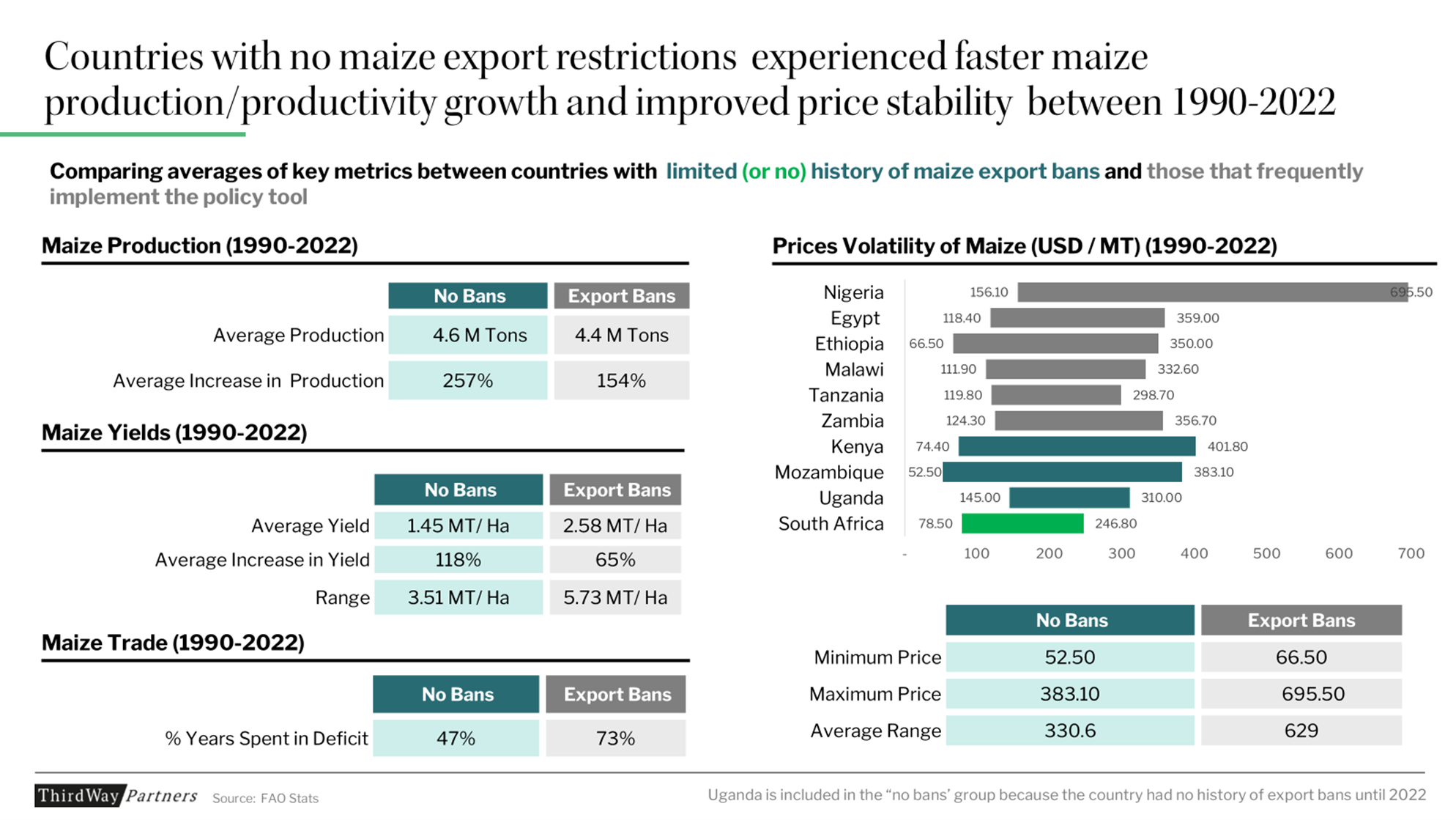

This is not only a pattern from our direct experience. A comparative analysis of nine African countries over three decades shows it clearly at a system level.

Countries without a history of export bans saw production growth 67% faster, yield increases nearly double, and average price ranges roughly half as wide as those with frequent discretionary interventions, across the same three-decade period.

Countries without a history of export bans saw production grow 257% on average, compared to 154% in countries that frequently applied them. Average yield increases were 118% versus 65%. Price ranges in ban countries were nearly twice as wide, a direct measure of the volatility that discretionary intervention creates. These differences are not explained by geography or starting conditions alone. They reflect the cumulative effect of predictable versus unpredictable operating environments on the investment and planting decisions of hundreds of thousands of farmers and traders over time.

Uganda offers a particularly sharp illustration. Following market liberalisation in the 1990s, Ugandan maize production grew at 5% per annum for nearly three decades. When the government introduced a temporary export ban in 2021, annual production dropped by 55%, yield by 92%, and the country recorded its first trade deficit since 2004. One episode of discretionary intervention, even a temporary one, was enough to reverse years of market development.

Rules-based systems support long-term planning

Rules-based frameworks do not eliminate risk, but they make risk more manageable. When market actors understand the conditions under which policies will be triggered, they can plan accordingly. That planning horizon is the foundation for the investment decisions that build agricultural market depth. This is particularly important in sectors characterised by seasonality and long investment cycles. Storage infrastructure, processing facilities, and export logistics all require upfront capital and extended planning horizons. Predictable rules reduce the risk premium attached to these investments which is another way of saying they make more of them viable.

Rules-based approaches also tend to produce better public sector outcomes. Clear frameworks reduce administrative burden, improve accountability, and limit the pressure on officials to make high-stakes decisions in real time under conditions of uncertainty.

What a mature rules-based system looks like

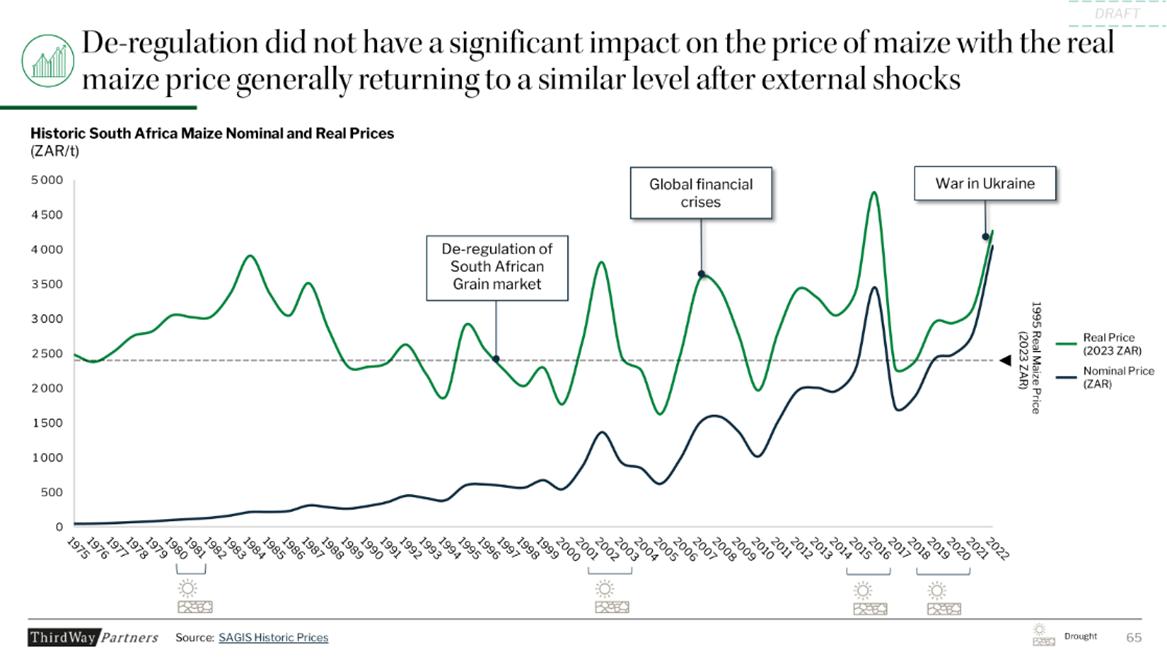

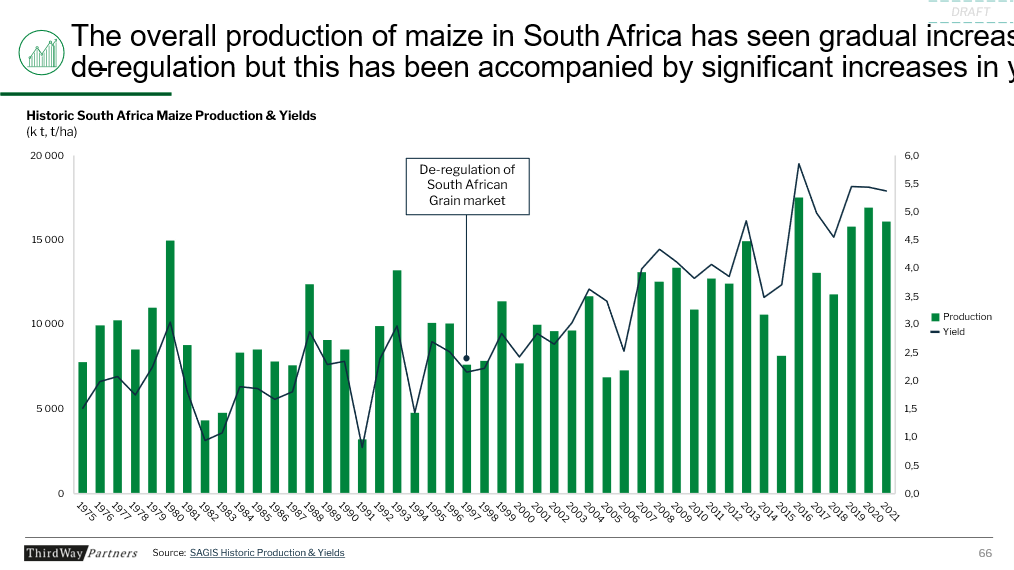

South Africa's grain market de-regulation, which began in the early 1990s, offers the clearest regional comparator for what rules-based reform looks like at maturity.

South Africa's real maize price (adjusted to 2023 ZAR) (First Image) has oscillated around a long-run mean since market de-regulation in the mid-1990s — absorbing the global financial crisis and the war in Ukraine without the persistent volatility that characterises heavily discretionary markets. Coupled with this, South Africa has constantly been able to grow its production and increase its yields during the same period (Second Image)

The chart is striking not for what it shows happening after de-regulation, but for what it shows not happening. Despite the global financial crisis, the 2015–16 drought, and the commodity shock from the war in Ukraine, the real price of maize returned to roughly the same long-run level each time. That is what resilience in a rules-based system looks like: not the absence of shocks, but the capacity to absorb them without structural disruption.

South Africa's 1996 Marketing of Agricultural Products Act went further than simply removing the floor price. It established the National Agricultural Marketing Council, defined clear and limited conditions under which the Minister could issue statutory measures, required public reasons for any decision to accept or reject the Council's recommendations, and created institutional architecture that gave private actors a stable and predictable operating environment. Predictability was designed in, not assumed.

Designing predictability into reform from the outset

Implementation-ready reform treats predictability as a core design principle rather than an outcome that will emerge naturally over time.

In practical terms, this means making explicit choices about where discretion is necessary and where rules should dominate. It means building in mechanisms to signal policy intent clearly and consistently, particularly during periods of market stress when the temptation to intervene is greatest. And it means designing triggers and thresholds that are transparent, measurable, and credible enough that private actors will rely on them when making long-term decisions.

Predictability does not mean inaction. It means that when governments intervene, they do so within frameworks that market actors understand and trust. That distinction, between arbitrary intervention and rule-governed action, is what separates markets that attract private capital from those that push it away.

Questions worth asking early

Reform processes that take predictability seriously tend to surface a different set of questions at the design stage:

Where in this sector are private actors currently absorbing policy risk, and how is that shaping their behaviour?

Which policy tools are rules-based, and which depend on discretionary judgement, and is that balance intentional?

What signals are market actors currently relying on, and do those signals accurately reflect government intent?

Where coordination across institutions or borders is needed, what mechanisms exist to maintain alignment over time?

What would it take for private actors to trust that the rules will hold?

Reforms that engage with these questions upfront are far more likely to translate into the investment and market development that food systems across the continent need.